Hi,

Just a short note to remind you to watch our summer "Encore" training webinars while you have the chance.

Take this opportunity to watch some of our BEST educational webinars - on demand.

Click below to listen in on these webinar topics:

>>> How to Invest in Apartments with No Cash, Credit, or Experience

>>> How to Get ALL the Money You'll Ever Need to Fund ALL Your Real Estate Deals

>>> How to Make $10,000 Finder's Fees in the Next 30 Days

>>> The Hidden Powers of LLCs for Real Estate to Protect Your Business & Family

>>> How to Get 3X Market Rent EVERY Month Guaranteed - No Landlording, No Hassles!

>>> How to Buy a House for $5,000 or Less Without Cash, Credit, or Experience

No need to register. They are free to attend. Just watch them "on demand" at your convenience.

Sincerely,

Jeanne Ekhaml, Publisher

Creative Real Estate Online

www.creonline.com

P.S. Don't forget... these "Encore" presentations end at midnight on Monday, September 5th.

CRE Online, Inc.

6440 Sky Pointe Dr.

Suite 140-187

Las Vegas, NV 89131

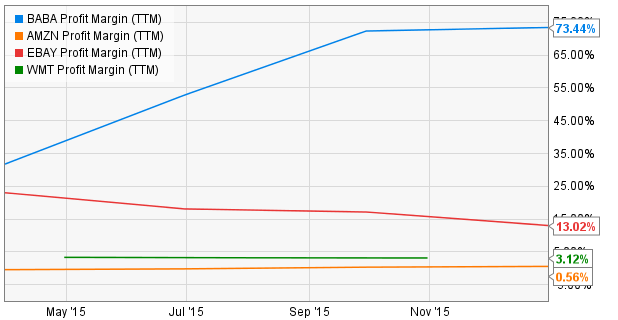

The story of Alibaba (NYSE:BABA) and its stock play is a fascinating one, but their success in China and in the e-retail space is even more gripping. As the most consistently profitable online retailer on the planet, Alibaba’s model deserves a second look. Why? After all, has not eBay (NASDAQ:EBAY) been successfully operating a marketplace portal all these years? What makes Alibaba so different?

The first difference, of course, is their profitability. Even though eBay finally breached the 25% operating profit margin barrier during the last fiscal, to say that Alibaba’s performance outshone them in that regard would be a gross understatement.

- Warning! GuruFocus has detected 4 Warning Signs with BABA. Click here to check it out.

- BABA 15-Year Financial Data

- The intrinsic value of BABA

- Peter Lynch Chart of BABA

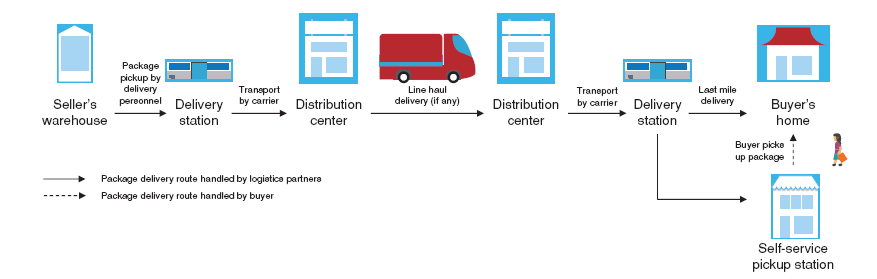

The second difference is the way they handle their shipping. In contrast to what most retailers including Amazon (NASDAQ:AMZN) and eBay do, Alibaba believes in letting others do the job, while providing the technology that closely monitors the status of each package shipped. Their subsidiary Cainiao Logistics does that part, and buyers get the option of picking the shipping company they want delivering their package.

This model not only makes it more transparent for the buyer as well as the seller, but more importantly, it completely eliminates the last-mile delivery expense that other online retailers struggle with as the cost of doing business.

And that is one of the reasons why Alibaba has been able to post this kind of profitability quarter after quarter since well before its IPO.

It is in the Valuation

Though revenues have been growing at a hectic pace, Alibaba stock was moving sideways for a while before it gained a second wind in February. This is despite revenues jumping to 101 billion Chinese yuan ($15.1 billion) from half that figure two years ago.

But the phenomenon is not inexplicable. In a recent article, I covered the post-IPO movement of Alibaba’s stock, and pointed out that in December 2013 the company was valuing itself at more than 18 times sales, and that investors had pushed that up by a further 40% or so.

Now let’s take a look at how they compare with Amazon on that front.

The Seattle-based e-commerce giant is trading at 3.1 times sales, despite being the leader in nearly every country they’ve entered so far except China. In India, after three short years they displaced Flipkart to take the number one spot, and continue to grow that market aggressively, recently introducing Amazon Prime.

Alibaba, on the other hand, is still trading at 14.7 times sales despite being a one-country player. On the growth front, these two companies are not that far apart. Amazon has been doubling its revenues every three years, while Alibaba has been doing it in two. But why this glaring disparity represented by a 5X difference in the price to sales ratios?

In fact, despite its reach, Amazon possibly has a much longer growth runway than Alibaba. Think about China’s dealings with foreign companies and how they arm-twist international players so their own domestic businesses always get the better end of the deal. As a result of this and other factors, Alibaba is going to have a hard time entering any developed market. And that is why Amazon will grow stronger as Alibaba makes the best of the Chinese market. To be fair, Alibaba does have ample room to grow within China, as internet penetration continues to increase. But after ten years in the business, do not you think it is odd that Alibaba has not taken any serious steps to enter any of the developed markets where a lot of its sellers are from?

To top it off, Alibaba does not have the kind of moat that Amazon does. It neither sells products nor ships them, which gives them a very weak USP when entering a new market. Of course they can set themselves up as a gateway to Chinese products, but they will lack the credibility that Amazon does wherever they go.

But let’s look at this from a valuation perspective to see why Alibaba’s upside is pretty much fully priced in.

Eight Years From Now…

Valued at slightly under a quarter of a trillion dollars in 2016, Alibaba’s revenues of near $15 billion give it P/S ratio of about 15, or thereabouts. On the other hand, Amazon’s $107 billion revenues last year gave them a P/S ratio of around 3, giving them a market cap of $320+ billion.

Now, fast forward eight years from now and assume that they hit Amazon’s current revenue level of $107 billion. Let’s also assume that their P/S adjusts itself to Amazon’s ratio of 3. That will give Alibaba a market cap similar to Amazon’s $320+ billion. So that’s a 4% compound annual growth rate for a period of eight years from their current market cap of $240+ billion.

Now, as Alibaba’s sales go up during that time, the valuation will keep correcting itself downwards. That means the margin of safety for investing is minimal. Of course, since China still holds ample opportunity for Alibaba to keep growing, their stock is also edging upwards. However, that is not a 20-year growth runway like Amazon has. Even an optimistic view will see BABA moving sideways or slowing creeping upwards over time.

As such, I would not recommend jumping into BABA with both feet. If you must invest in China’s biggest e-tailer, then add to your position over several years. Remember, there is very little room for error so practice the utmost caution. And do not expect to walk away in a few years’ time with hefty returns. This will be a slow journey that lasts several years, but in the end, you will get your return.

Disclosure: I have no positions in any of the stocks mentioned above and no intention to initiate a position in the next 72 hours.

Start a free 7-day trial of Premium Membership to GuruFocus.